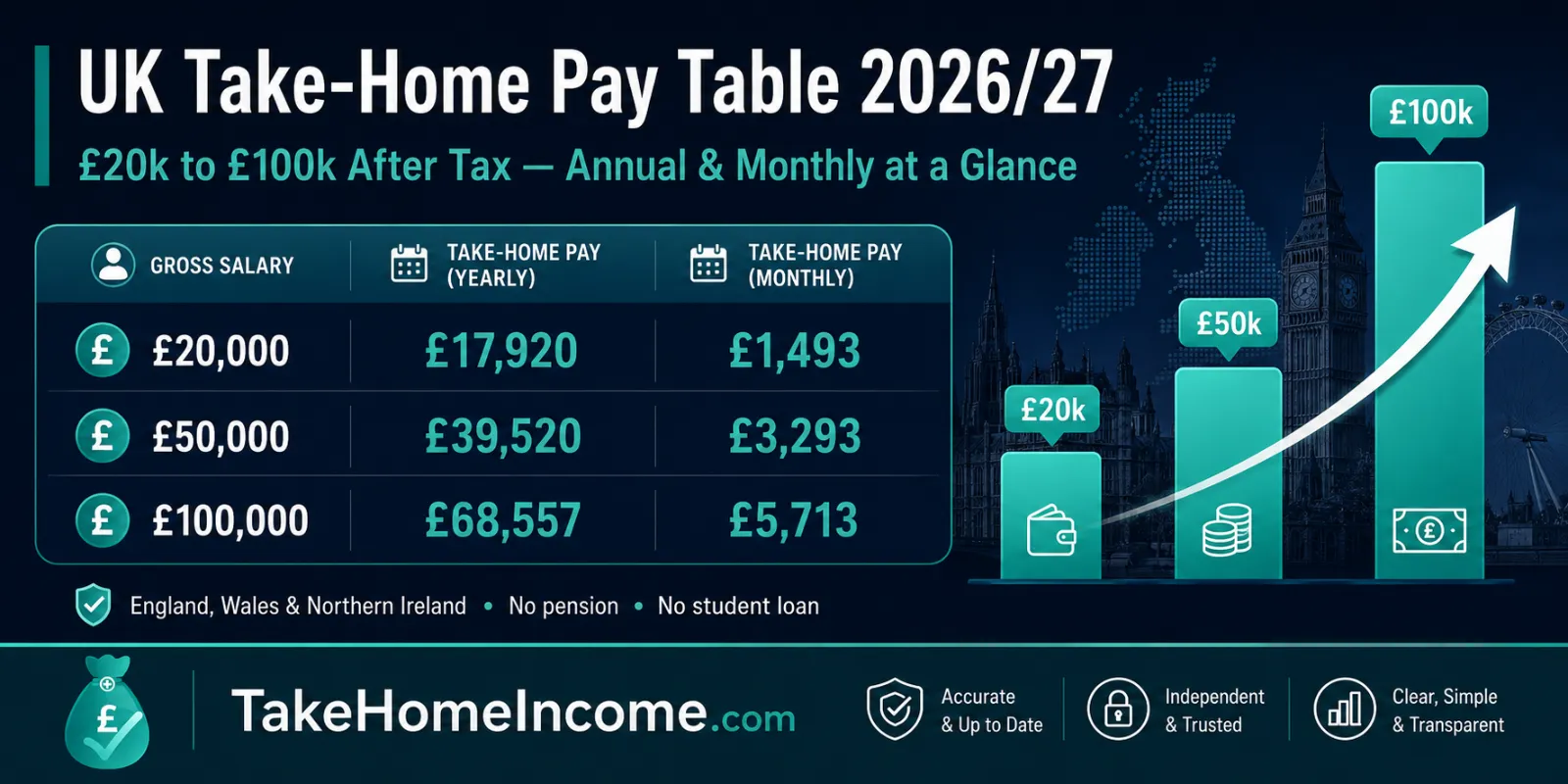

This is a complete salary after tax comparison table for the UK in the 2026/27 tax year (6 April 2026 to 5 April 2027). On a £20,000 salary you keep about £17,920 a year (roughly £1,493 a month); on £50,000 about £39,520 (£3,293 a month); and on £100,000 about £68,557 (£5,713 a month). Every figure below is for a standard Category A employee in England, Wales or Northern Ireland, with no pension contribution and no student loan, calculated straight from the published HMRC and GOV.UK rates.

Use this page as a quick reference, then jump to a single-salary breakdown or run your exact number in our UK salary after tax calculator.

UK take-home pay table: £20k to £100k (2026/27)

The table shows gross salary, annual net pay, monthly net pay, total deductions (Income Tax + National Insurance) and the effective rate (the share of your whole salary lost to tax and NI), plus the percentage you keep. Figures are England/rUK and are rounded to the nearest pound.

| Gross salary | Annual take-home | Monthly take-home | Total deductions | Effective rate | % kept |

|---|---|---|---|---|---|

| £20,000 | £17,920 | £1,493 | £2,080 | 10.4% | 89.6% |

| £25,000 | £21,520 | £1,793 | £3,480 | 13.9% | 86.1% |

| £30,000 | £25,120 | £2,093 | £4,880 | 16.3% | 83.7% |

| £35,000 | £28,720 | £2,393 | £6,280 | 17.9% | 82.1% |

| £40,000 | £32,320 | £2,693 | £7,680 | 19.2% | 80.8% |

| £45,000 | £35,920 | £2,993 | £9,080 | 20.2% | 79.8% |

| £50,000 | £39,520 | £3,293 | £10,480 | 21.0% | 79.0% |

| £55,000 | £42,457 | £3,538 | £12,543 | 22.8% | 77.2% |

| £60,000 | £45,357 | £3,780 | £14,643 | 24.4% | 75.6% |

| £65,000 | £48,257 | £4,021 | £16,743 | 25.8% | 74.2% |

| £70,000 | £51,157 | £4,263 | £18,843 | 26.9% | 73.1% |

| £75,000 | £54,057 | £4,505 | £20,943 | 27.9% | 72.1% |

| £80,000 | £56,957 | £4,746 | £23,043 | 28.8% | 71.2% |

| £85,000 | £59,857 | £4,988 | £25,143 | 29.6% | 70.4% |

| £90,000 | £62,757 | £5,230 | £27,243 | 30.3% | 69.7% |

| £95,000 | £65,657 | £5,471 | £29,343 | 30.9% | 69.1% |

| £100,000 | £68,557 | £5,713 | £31,443 | 31.4% | 68.6% |

Monthly figures are simply the annual take-home divided by 12. Your own payslip can differ slightly because PAYE spreads tax across the year and because pension, student loan, benefits and your tax code all change the result.

How do I read the table: gross vs net vs % kept?

Three numbers do most of the work:

- Gross salary – the headline figure in your contract, before anything is taken off.

- Net (take-home) pay – what actually lands in your bank account after Income Tax and National Insurance.

- Effective rate – total deductions divided by gross salary. It is always lower than your top tax band, because your first £12,570 is tax-free and lower slices are taxed at lower rates.

The % kept column is just 100% minus the effective rate. Notice it falls steadily as salary rises: you keep almost 90% of a £20,000 salary but under 69% of a £100,000 one. That is the tax system working exactly as designed – higher slices of income are taxed at higher rates.

Where do the tax bands bite in 2026/27?

Four thresholds shape every row in the table. Knowing them explains why take-home grows quickly at the bottom and slows down higher up.

| Threshold | What happens | Marginal effect |

|---|---|---|

| £12,570 | Personal Allowance ends; Income Tax and employee NI both begin | 0% → 28% (20% tax + 8% NI) |

| £50,270 | Higher-rate (40%) band starts; NI drops to 2% | 28% → 42% (40% tax + 2% NI) |

| £100,000 | Personal Allowance starts tapering (−£1 per £2) | 42% → about 62% |

| £125,140 | Personal Allowance fully gone; 45% additional rate begins | 62% → 47% (45% tax + 2% NI) |

The band edges are based on the full £12,570 Personal Allowance: the 20% basic-rate band runs to £50,270, the 40% higher-rate band to £125,140, and the 45% additional rate applies above that. The official figures are published by HMRC on GOV.UK.

Basic-rate salaries (£20k–£50k): what changes as you climb?

Across this whole range you sit in the 20% basic-rate band and pay 8% National Insurance, so every extra £1,000 of salary is taxed the same way and adds the same £720 to your take-home. That is why the rows step up so evenly.

Take a £40,000 salary. Your taxable income is £40,000 − £12,570 = £27,430.

- Income Tax: 20% of £27,430 = £5,486

- National Insurance: 8% of £27,430 = £2,194

- Total deductions: £7,680 → take-home £32,320 a year (about £2,693 a month)

Because the NI Primary Threshold (£12,570) now matches the Personal Allowance, the same £27,430 slice carries both taxes. The effective rate climbs from 10.4% at £20k to 21.0% at £50k – still comfortably below the 28% headline because of that tax-free first slice.

A lower salary works the same way with a smaller taxed slice. On £25,000 your taxable income is £12,430, so Income Tax is 20% of that (£2,486) and NI is 8% of that (£994). Total deductions are £3,480, leaving £21,520 a year (about £1,793 a month) and an effective rate of just 13.9%. The key insight for this whole band: your take-home rises in a straight line, so you can read off any in-between salary by interpolating between two rows – each £1,000 is worth exactly £720 net, or £60 a month.

Higher-rate salaries (£50k–£100k): the 40% band and the taper

Once you pass £50,270, two things happen at once: income above that point is taxed at 40%, but National Insurance drops from 8% to 2%. So each extra £1,000 in this band is taxed at a combined 42% and adds £580 to take-home – less than the £720 a basic-rate earner keeps, which is why the rows step up more slowly from £55k onward.

For a £60,000 salary in England:

- Income Tax: 20% on £37,700 (£7,540) + 40% on £9,730 (£3,892) = £11,432

- National Insurance: 8% on £37,700 (£3,016) + 2% on £9,730 (£195) = £3,211

- Take-home: £45,357 a year (about £3,780 a month)

The £100,000 mark is where it gets harsh. Above it, every £2 of income removes £1 of Personal Allowance, so a slice that was tax-free becomes taxed at 40%. Between £100,000 and £125,140 the effective marginal rate is around 60% on Income Tax (about 62% with NI) – the well-known "£100k trap". That band sits just past the top of this table, but it is why many earners near £100k pay extra into a pension to stay under the line.

How does the table change for Scottish taxpayers?

Scotland sets its own Income Tax (National Insurance is identical UK-wide), with six bands from 19% to 48%. Lower earners pay slightly less than in England thanks to the 19% starter rate; middle and higher earners pay more, because the higher rate is 42% (not 40%) and starts earlier, at £43,663. Here is the same salary range under Scottish bands.

| Gross salary | Annual take-home (Scotland) | Monthly take-home | Effective rate | vs England |

|---|---|---|---|---|

| £20,000 | £17,959 | £1,497 | 10.2% | +£40 |

| £30,000 | £25,155 | £2,096 | 16.2% | +£35 |

| £40,000 | £32,255 | £2,688 | 19.4% | −£65 |

| £50,000 | £38,024 | £3,169 | 23.9% | −£1,496 |

| £60,000 | £43,607 | £3,634 | 27.3% | −£1,750 |

| £80,000 | £54,657 | £4,555 | 31.7% | −£2,300 |

| £100,000 | £65,257 | £5,438 | 34.7% | −£3,300 |

The crossover sits around £30,000–£31,000: below it a Scottish taxpayer keeps a touch more, above it they keep less, and the gap widens with income. At £50,000 a Scottish taxpayer takes home roughly £1,500 less per year than someone on the same salary in England, largely because the higher rate bites from £43,663 rather than £50,270.

How do pension and student loan move every row?

The headline table assumes no pension and no student loan. Both shift every figure, in opposite directions:

- Workplace pension (salary sacrifice): a contribution is taken before tax and NI, so your take-home falls by less than the amount paid in. A 5% contribution on £40,000 is £2,000, but because you save 20% tax and 8% NI on that slice, take-home drops by only about £1,440.

- Student loan: repayments are 9% of income above your plan threshold (6% for a Postgraduate Loan). Thresholds for 2026/27 are Plan 1 £26,900, Plan 2 £29,385, Plan 4 £33,795, Plan 5 £25,000 and Postgraduate £21,000. On a £40,000 Plan 2 salary that is 9% of £10,615 = about £955 a year off your take-home.

Because these depend on your exact plan and contribution rate, the only way to get a precise figure is to enter them. The salary after tax calculator applies your region, pension, student loan and pay frequency in one go.

What salary do I need to take home £2,000 a month?

To clear £2,000 a month (£24,000 a year) after tax in England, you need a gross salary of about £28,400–£28,500. That is comfortably inside the basic-rate band, so the maths is straightforward: each extra £1,000 of salary adds £720 to take-home, or £60 a month. To target a different monthly figure, find the nearest row above and below in the table and interpolate, or just type the monthly target into the calculator’s reverse (net-to-gross) mode.

Why might my payslip differ from the table?

The table is an annualised, whole-year calculation – it matches what your P60 should show at year end. A single payslip can read a little differently for several normal reasons:

- Your tax code. The figures assume the standard 1257L code (the full £12,570 allowance). A different code – for a company benefit, underpaid tax from a previous year, or a second job – changes how much is taxed.

- PAYE timing. Pay As You Earn spreads your allowance evenly across 12 months. A bonus or a pay rise mid-year can be over-taxed in one month and corrected later, so individual payslips wobble even though the yearly total matches.

- Benefits in kind. A company car, private medical cover or other P11D benefits are taxed through your code. They raise your Income Tax (and can trigger the High Income Child Benefit Charge) but carry no employee National Insurance and are not part of your cash take-home.

- Pension and student loan. As covered above, both move every row, and the exact amount depends on your contribution rate and loan plan.

For any of these, the quickest path to an accurate figure is to enter your own details rather than read off a round-number row.

Jump to a single-salary breakdown or run your own number

This page is a hub. Once you have spotted your salary in the table, you can dig into a dedicated breakdown for popular figures – for example £30k, £40k, £50k, £60k or £100k after tax – or skip straight to a precise, personalised result. The UK salary after tax calculator handles region (including Scotland), pension, student loan plan, pay frequency and your tax code, and shows every deduction line by line for 2026/27.

Key takeaways

- In 2026/27, England/rUK take-home runs from about £17,920 on £20k to £68,557 on £100k – roughly £1,493 to £5,713 a month.

- The % you keep falls from 89.6% to 68.6% across that range, because higher slices are taxed at higher rates.

- The 40% higher-rate band starts at £50,270; at the same point NI drops from 8% to 2%, so the combined marginal rate is 42%.

- Each extra £1,000 adds £720 to take-home in the basic-rate band but only £580 in the higher-rate band.

- Scotland lets lower earners keep slightly more, but charges middle and higher earners more – about £1,500 less take-home at £50k.

- The £100,000–£125,140 taper creates an effective marginal rate near 60% on Income Tax (about 62% with NI).