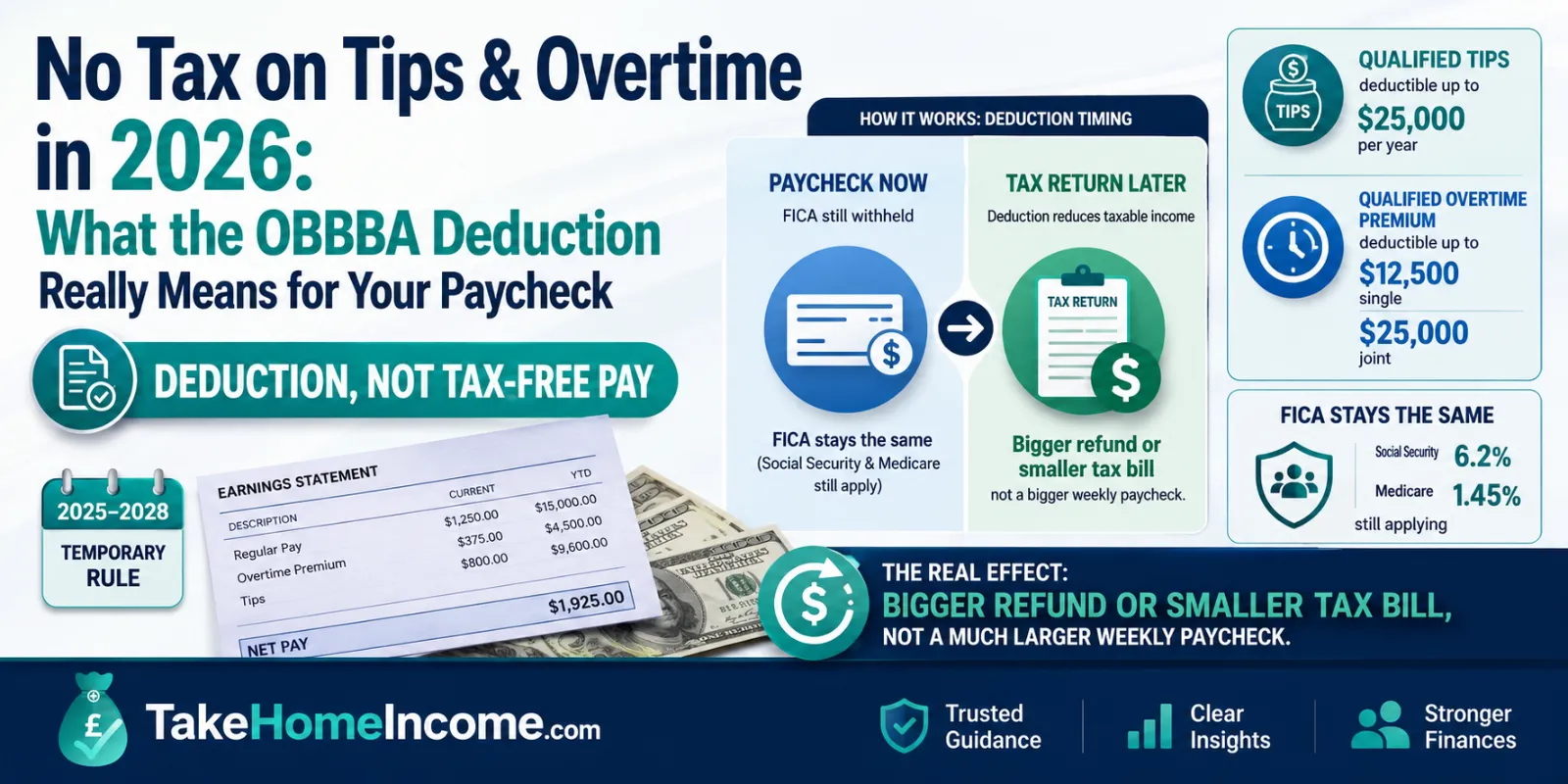

“No tax on tips and overtime” in 2026 is an income-tax deduction, not a payroll-tax exemption. Under the One Big Beautiful Bill Act (OBBBA), you can deduct up to $25,000 of qualified tips and up to $12,500 of qualified overtime ($25,000 if married filing jointly) when you file your federal return. But Social Security, Medicare and your normal federal withholding are unchanged, so this shows up as a bigger refund or smaller tax bill at filing time, not as a fatter weekly paycheck.

The headline “no tax on tips” has been widely misread as “tips are now tax-free.” They are not. The IRS and Social Security Administration (SSA) still treat every tipped dollar and every overtime dollar as wages for payroll-tax purposes. What OBBBA created (new Internal Revenue Code §224 for tips and §225 for overtime) are two new above-the-line deductions that reduce your taxable income for the 2025 through 2028 tax years. This guide pins down exactly what qualifies, the dollar caps, the income phase-outs, and the difference between what changes on your paycheck and what changes on your tax return.

No tax on tips and overtime: what it actually is

OBBBA, signed in July 2025, did not exempt tips or overtime from tax. It added two temporary deductions:

- A deduction, not an exemption. The amount comes off your taxable income on Form 1040, the same place the standard deduction sits. It lowers the income your federal income tax is calculated on.

- Available to non-itemizers. You can claim it whether or not you itemize, so the roughly 90% of filers who take the standard deduction can still benefit.

- Federal only. It changes federal income tax. It does not touch Social Security tax, Medicare tax, or state and local income taxes, those still apply to the full amount.

- Temporary. It applies to tax years 2025, 2026, 2027 and 2028, then expires unless Congress extends it.

- Claimed on your return. You take it when you file, so the benefit arrives as a refund or a lower balance due, not as extra money in each pay period.

That last point is the one workers most often get wrong, so we cover it in detail below.

How does the no-tax-on-tips deduction work?

The tips deduction (IRC §224) lets eligible workers deduct their qualified tips, up to a cap of $25,000 per tax return. Key rules:

- Cap of $25,000. This is per return, regardless of filing status, a married couple who both earn tips still share a single $25,000 ceiling.

- Qualified tips only. These are voluntary cash or charged tips from customers, including tips shared through a valid tip-pool. Mandatory service charges and automatic gratuities (the “18% added for parties of six”) do not count, legally those are wages, not tips.

- Tipped occupations only. You must work in an occupation that customarily and regularly received tips on or before December 31, 2024. The IRS published the qualifying occupation list (servers, bartenders, hairstylists, delivery drivers, valets and more). Each is tied to a Treasury Tipped Occupation Code (TTOC).

- Some high earners are blocked. Self-employed people in a “specified service trade or business” (SSTB), think doctors, lawyers, accountants, cannot use the tips deduction, and for the self-employed it can’t exceed your net business income.

You report your tips as normal; the deduction is then calculated from the qualified-tip figure your employer reports (or that you self-report on Form 4137 for unreported tips).

How does the no-tax-on-overtime deduction work?

The overtime deduction (IRC §225) is narrower than most people expect. It applies only to the “premium” portion of overtime, the extra half of time-and-a-half required under the federal Fair Labor Standards Act (FLSA), not your whole overtime cheque.

- Only the half-time premium counts. If your regular rate is $30/hour and overtime pays $45/hour (time-and-a-half), only the $15 premium per overtime hour is deductible, not the full $45.

- Cap of $12,500 ($25,000 joint). A single filer can deduct up to $12,500 of qualified overtime premium; married-filing-jointly couples up to $25,000.

- FLSA overtime only. It covers overtime that the FLSA requires at one-and-a-half times the regular rate. Contractual “double-time” above that, or daily overtime your state mandates beyond federal rules, may not all qualify.

So a worker who books a lot of overtime hours gets a real but bounded benefit, capped, and only on the premium slice.

Worked example: a tipped server on $40,000

Take a single restaurant server in 2026 earning $40,000 total, of which $18,000 is qualified cash tips. Their income is well below the phase-out, and $18,000 is under the $25,000 cap, so the full $18,000 is deductible.

- FICA, unchanged. Social Security 6.2% × $40,000 = $2,480; Medicare 1.45% × $40,000 = $580. Total FICA = $3,060, exactly the same as if there were no tips deduction at all.

- Income tax without the deduction: taxable income = $40,000 − $16,100 standard deduction = $23,900. Tax = 10% × $12,400 + 12% × ($23,900 − $12,400) = $1,240 + $1,380 = $2,620.

- Income tax with the $18,000 tips deduction: taxable income = $40,000 − $16,100 − $18,000 = $5,900. Tax = 10% × $5,900 = $590.

- Federal income-tax saving = $2,620 − $590 = $2,030.

Notice the saving is $2,030, not $18,000. A deduction saves you tax at your marginal rate, not dollar-for-dollar. Here the top $11,500 of tips was being taxed at 12% and the next $6,500 at 10%, so the benefit is 12% × $11,500 + 10% × $6,500 = $2,030. Sanity check: $590 + $2,030 = $2,620. ✓

Worked example: 100 hours of overtime

A single worker with a $30/hour regular rate works 100 overtime hours at time-and-a-half ($45/hour) during 2026:

- Overtime pay received = 100 × $45 = $4,500, and all $4,500 is still subject to Social Security, Medicare and federal withholding.

- Deductible premium = the extra $15/hour × 100 = $1,500 (the FLSA “half”), comfortably under the $12,500 cap.

- At a 12% marginal rate, the income-tax saving is 12% × $1,500 = $180 at filing time.

Real money, but modest, and only on the premium, not the full overtime amount.

What is the MAGI phase-out at $150k / $300k?

Both deductions shrink for higher earners. They phase out by $100 for every $1,000 that your modified adjusted gross income (MAGI) exceeds:

- $150,000 for single filers, and

- $300,000 for married filing jointly.

So a single filer with MAGI of $160,000 is $10,000 over the threshold, reducing the maximum deduction by $1,000 (10 × $100). The deductions fully disappear well before the very top of the income scale, this is a benefit aimed squarely at lower- and middle-income workers, which is exactly who earns most tips and overtime.

Does no tax on tips change my paycheck withholding?

No, your paycheck math is essentially unchanged. This is the single most misunderstood point. Tips and overtime remain fully subject to:

- Social Security tax, 6.2% on wages up to the 2026 wage base of $184,500.

- Medicare tax, 1.45% on all wages, plus an extra 0.9% Additional Medicare Tax above $200,000 (single).

- Federal income-tax withholding, your employer keeps withholding under the normal tables; the deduction is settled when you file, not at the till.

- State and local income taxes, most states have not adopted a matching break, so they still tax the full amount (check your own state).

Here is the framing workers actually search for, what changes on your paycheck versus on your tax return:

| Item | On your paycheck (each pay period) | On your tax return (when you file) |

|---|---|---|

| Social Security & Medicare (FICA) | No change, charged on full tips & overtime | No change |

| Federal income-tax withholding | Largely unchanged, employer uses normal tables | Deduction lowers taxable income |

| Qualified tips (up to $25,000) | Still taxed/withheld as normal | Deducted, lowers federal tax |

| Qualified overtime premium ($12,500 / $25,000 joint) | Still taxed/withheld as normal | Deducted, lowers federal tax |

| State & local income tax | No change (most states) | Usually no change |

| Where you feel it | , | Bigger refund / smaller balance due |

Do I still pay Social Security and Medicare on tips and overtime?

Yes. The deduction is for income tax only. The IRS is explicit that Social Security and Medicare taxes continue to apply to tip income and to overtime, for both you and your employer. That matters beyond your paycheck: because you keep paying into Social Security on your tips and overtime, those earnings still count toward your future Social Security benefit. A genuine payroll-tax exemption would have quietly lowered the retirement benefits of tipped and overtime workers; a deduction does not.

Paycheck vs refund: where do you actually see the benefit?

Because the deduction is claimed on your annual return, the benefit lands as a refund or reduced tax bill the following spring, not as a larger paycheck during the year. Two practical implications:

- If you want the cash sooner, you could adjust your Form W-4 (e.g. claim the expected deduction so less is withheld), but that risks under-withholding if your tips or hours fall, so tread carefully.

- If you do nothing, you’ll simply get a bigger refund. For the server in our example, that’s roughly $2,030 extra back at tax time; for the overtime worker, about $180.

For tax year 2025 specifically, the W-2 boxes weren’t updated in time, so the IRS allowed transition relief and posted guidance on how to identify your qualified amounts. From 2026 onward, reporting is built into the W-2 (next section), making the figures easier to find.

New W-2 reporting boxes for tips and overtime

Starting with amounts earned in 2026, employers report the new figures directly on your Form W-2, so you (and the IRS) can see exactly what qualifies:

| Amount | Where it appears on the 2026 W-2 |

|---|---|

| Qualified tips | Box 12, code TP |

| Treasury Tipped Occupation Code (TTOC) | Box 14b |

| Qualified overtime compensation | Box 12, code TT |

When you file, you (or your software) pull these amounts onto the return to claim the deductions. Always reconcile the W-2 figures against your own pay records, only the qualifying portions (cash tips, the FLSA overtime premium) should appear.

Key takeaways

- It’s a deduction, not an exemption. “No tax on tips and overtime” lowers your federal taxable income; it does not make tips or overtime tax-free.

- Caps: qualified tips up to $25,000 per return; qualified overtime premium up to $12,500 single / $25,000 joint.

- Overtime = the premium only. Just the “half” of time-and-a-half qualifies, not your whole overtime cheque.

- Phase-outs: reduced by $100 per $1,000 of MAGI above $150,000 single / $300,000 joint.

- FICA is unchanged. You still pay 6.2% Social Security (up to the $184,500 wage base) and 1.45% Medicare on every tipped and overtime dollar, and it still builds your Social Security record.

- You feel it at filing, as a bigger refund or smaller bill, not in each paycheck.

- Temporary: tax years 2025–2028, per the OBBBA (IRC §§224–225).

- 2026 W-2: tips in Box 12 code TP (TTOC in Box 14b); overtime in Box 12 code TT.

Estimate your take-home with tips or overtime

Because the deduction is income-tax only and capped, the easiest way to see your real number is to model your full wages first. Our US salary after tax calculator applies the 2026 federal brackets, the $16,100 standard deduction and FICA (Social Security to the $184,500 wage base, plus Medicare) line by line. Enter your total pay including tips and overtime to see your baseline take-home; then subtract your qualified tips (up to $25,000) and overtime premium (up to $12,500 / $25,000 joint) from taxable income, multiply by your marginal rate, and that’s your expected extra refund, just like the worked examples above.