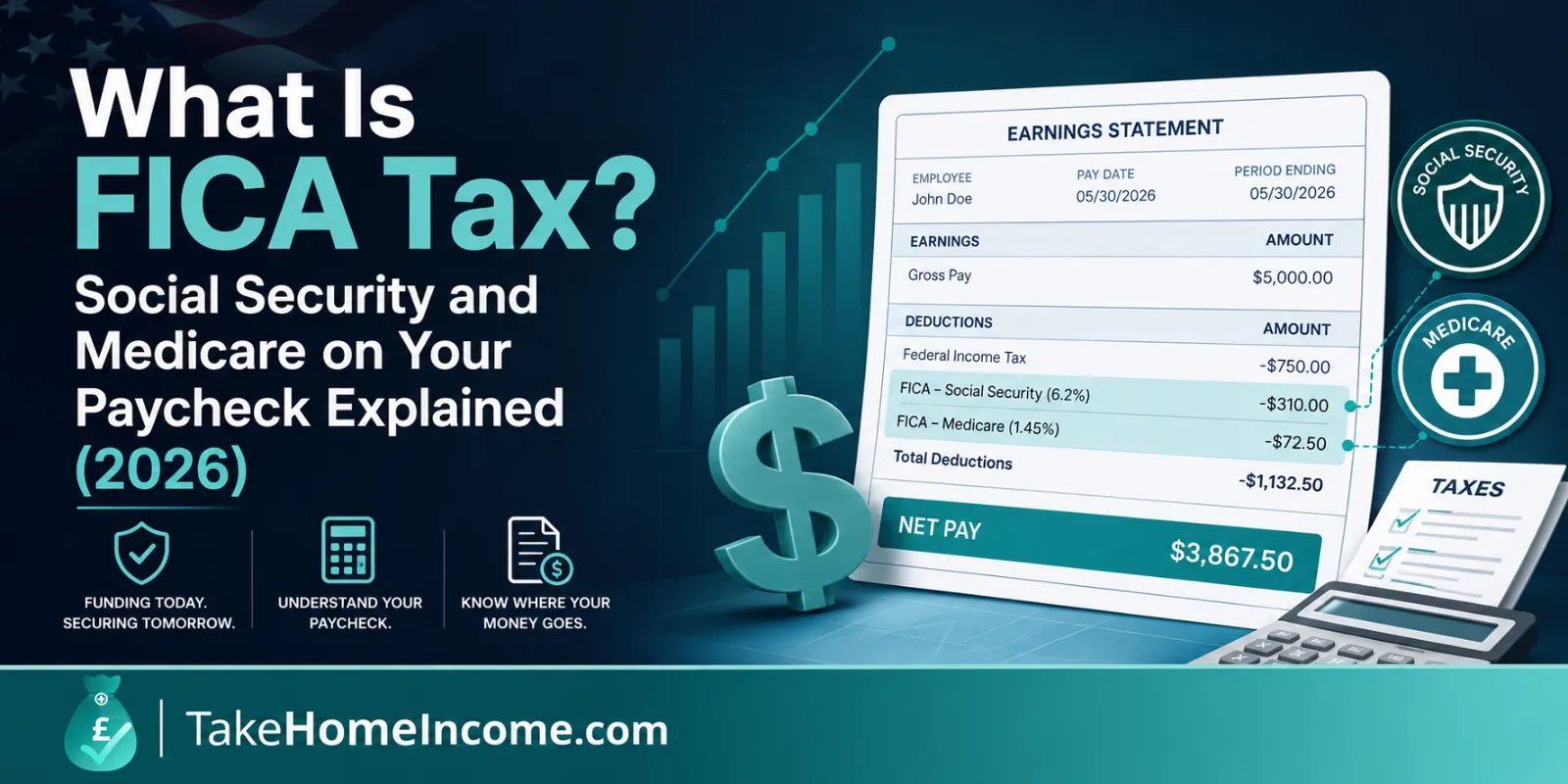

FICA is the combination of two federal payroll taxes, Social Security (6.2%) and Medicare (1.45%); that together take 7.65% out of your paycheck. If you have ever squinted at a pay stub and wondered what the “FICA” line means, that one-liner is the whole answer: FICA = 6.2% Social Security + 1.45% Medicare = 7.65%. For 2026, the 6.2% Social Security piece applies only up to a wage base of $184,500, while the 1.45% Medicare piece applies to every dollar you earn.

FICA stands for the Federal Insurance Contributions Act, the 1935 law that funds Social Security and Medicare through payroll taxes. It is separate from federal income tax: income tax pays for general government, while FICA is earmarked for two specific benefit programs. This guide breaks down each component, the 2026 rates and caps from the IRS and the Social Security Administration (SSA), why your employer pays a matching share you never see, and exactly what FICA costs on a typical salary.

What is FICA tax in one line?

FICA is the payroll tax that funds Social Security and Medicare. It has two parts, and as an employee you pay both:

- Social Security tax (OASDI); 6.2% of your wages, up to an annual wage base ($184,500 in 2026). This funds retirement, disability and survivor benefits.

- Medicare tax (Hospital Insurance); 1.45% of all your wages, with no cap. This funds Medicare Part A hospital coverage.

Add them up and the standard employee FICA rate is 6.2% + 1.45% = 7.65%. That is the number withheld from each paycheck before you ever see the money, on top of, and separate from, federal income tax.

Almost every W-2 employee in the United States pays FICA, and it starts from the very first dollar of wages; there is no tax-free threshold and no standard deduction for FICA the way there is for income tax. Tips, bonuses, commissions and most taxable fringe benefits all count as FICA wages too, so the 7.65% reaches more of your compensation than you might expect.

What is the FICA tax rate for 2026?

The combined employee FICA rate for 2026 is 7.65%. Here is how it splits, along with the cap on each component:

| Component | Employee rate | 2026 cap / threshold |

|---|---|---|

| Social Security (OASDI) | 6.2% | On wages up to $184,500 |

| Medicare (Hospital Insurance) | 1.45% | No cap, all wages |

| Standard FICA total | 7.65% | , |

| Additional Medicare Tax | +0.9% | On wages over $200,000 (single) |

The 6.2% and 1.45% rates have not changed for 2026; they are set in statute and rarely move. What changes most years is the Social Security wage base, which the SSA adjusts for inflation. For 2026 that base rose to $184,500.

What is the Social Security wage base for 2026, and where does the tax stop?

The 2026 Social Security wage base is $184,500. That is the maximum amount of earnings subject to the 6.2% Social Security tax in a year. Earn above it and the extra wages are not taxed for Social Security, though Medicare keeps applying.

This gives one of the most precise, quotable numbers in all of US payroll: the most Social Security tax an employee can pay in 2026 is

- $184,500 × 6.2% = $11,439.00

Once your year-to-date wages cross $184,500, the 6.2% Social Security line on your pay stub drops to zero for the rest of the year. High earners often notice a small bump in take-home pay late in the year for exactly this reason. (Your employer’s matching 6.2% also stops at the same point.)

How does Medicare tax work and what is the 0.9% surtax?

Medicare is the simpler half: 1.45% of every dollar you earn, with no wage base or ceiling. Whether you make $30,000 or $3 million, the first 1.45% of Medicare tax applies to all of it.

On top of that, higher earners pay an Additional Medicare Tax of 0.9% on wages above a filing-status threshold. These thresholds are written into the law and are not adjusted for inflation, so they are the same every year:

| Filing status | Additional Medicare Tax threshold |

|---|---|

| Single | $200,000 |

| Married filing jointly | $250,000 |

| Married filing separately | $125,000 |

| Head of household | $200,000 |

The extra 0.9% applies only to the wages above the threshold, not your whole salary. So a single filer earning $250,000 pays the surtax on $250,000 − $200,000 = $50,000, which is 0.9% × $50,000 = $450. Below $200,000 (single), the Additional Medicare Tax is $0, and your Medicare rate is just the flat 1.45%. Note that employers must start withholding the 0.9% once your pay with them passes $200,000, regardless of filing status, any over or under-withholding is reconciled on your tax return.

Why does my employer also pay FICA?

FICA is a shared tax. For every dollar of Social Security and Medicare tax you pay, your employer pays a matching amount, but that employer share is not deducted from your paycheck. You only ever see your half.

| Tax | You pay | Employer pays | Combined |

|---|---|---|---|

| Social Security | 6.2% | 6.2% | 12.4% |

| Medicare | 1.45% | 1.45% | 2.9% |

| Total FICA | 7.65% | 7.65% | 15.3% |

So the program is funded by a combined 15.3% of your wages (up to the Social Security cap), split evenly between you and your employer. The one exception to “you only pay half” is the 0.9% Additional Medicare Tax that surtax is paid by the employee only; employers do not match it.

A worked example: FICA on a $60,000 salary in 2026

Suppose you are a single filer earning $60,000 with no pre-tax deductions. Your FICA for the year is:

- Social Security: 6.2% × $60,000 = $3,720 (well under the $184,500 cap, so the full salary is taxed)

- Medicare: 1.45% × $60,000 = $870

- Total FICA: $3,720 + $870 = $4,590 for the year

That is 7.65% of $60,000, exactly as expected, about $382.50 a month, or roughly $176.54 from each biweekly paycheck. FICA is only part of the story, though. You also owe federal income tax, calculated separately on your income after the standard deduction:

- Taxable income: $60,000 − $16,100 standard deduction (single, 2026) = $43,900

- Federal income tax: 10% × $12,400 + 12% × ($43,900 − $12,400) = $1,240 + $3,780 = $5,020

Putting it together for a Florida or Texas resident (states with no income tax, so the numbers are pure federal):

| Line | Amount |

|---|---|

| Gross salary | $60,000 |

| Federal income tax | −$5,020 |

| FICA (Social Security + Medicare) | −$4,590 |

| Take-home pay | $50,390 |

That works out to about $4,199 a month. FICA alone is 7.65% of gross; add federal income tax and the combined bite here is about 16.0%. (Add a state income tax and your take-home would be lower; FICA itself is identical in every state.)

Self-employed? The FICA equivalent is SECA (15.3%)

If you work for yourself, there is no employer to split the bill with so you pay both halves under a parallel law called the Self-Employment Contributions Act (SECA). The self-employment tax rate is the full combined FICA rate:

- 12.4% Social Security (on net earnings up to the $184,500 wage base) + 2.9% Medicare (uncapped) = 15.3%

Two adjustments soften the blow. First, you only pay SECA on 92.35% of your net self-employment profit (this mirrors the fact that employees’ wages exclude the employer share). Second, you can deduct half of your SECA tax when figuring your federal income tax. For example, on $60,000 of net self-employment profit:

- Net earnings subject to SECA: $60,000 × 92.35% = $55,410

- Self-employment tax: 15.3% × $55,410 = $8,477.73

- Deductible half (reduces income tax): about $4,238.87

The same 0.9% Additional Medicare Tax also applies to self-employment income above the filing-status thresholds. If you are self-employed, our US salary after tax calculator is a useful starting point for understanding how Social Security and Medicare stack on top of federal income tax, though SECA-specific deductions are handled on your tax return.

What FICA does and doesn’t cover

It helps to be precise about what FICA is and what it is not:

- FICA is not federal income tax. Income tax uses graduated brackets and the standard deduction; FICA is a flat percentage from the first dollar (no deduction reduces the Medicare portion).

- Pre-tax 401(k) contributions still pay FICA. Traditional 401(k) money lowers your income tax but not your Social Security or Medicare tax. FICA is taken on your gross wages.

- HSA and pre-tax (Section 125) health premiums do reduce FICA. These come out before Social Security and Medicare are calculated, so they trim both your income tax and your FICA.

- FICA is not state tax. It is federal and identical in all 50 states; from no-income-tax states like Florida, Texas, Washington and Nevada to high-tax states like California and New York.

Key takeaways

- FICA = 6.2% Social Security + 1.45% Medicare = 7.65% of your pay, withheld from every paycheck and separate from federal income tax.

- The 2026 Social Security wage base is $184,500; the most Social Security tax an employee pays is $184,500 × 6.2% = $11,439.00. Above that, the 6.2% stops.

- Medicare is 1.45% on all wages with no cap, plus a 0.9% Additional Medicare Tax on wages over $200,000 (single) or $250,000 (married filing jointly).

- Your employer matches your 7.65%, so the program is funded by a combined 15.3%, but the match is not deducted from your check (the 0.9% surtax is employee-only).

- On a $60,000 salary, FICA is $4,590 a year ($3,720 Social Security + $870 Medicare), about $382.50 a month.

- Self-employed workers pay the full 15.3% as SECA on 92.35% of net profit, and can deduct half against income tax.

See your FICA and full take-home pay

FICA is just one of the deductions on your paycheck; federal income tax, and in most states a state income tax, sit alongside it. To see exactly how Social Security, Medicare and income tax combine for your salary, filing status and pre-tax contributions, run your numbers through our US salary after tax calculator. It applies the 2026 federal rules and the $184,500 Social Security wage base automatically and breaks out every line, so you can see your FICA and your true take-home pay side by side.