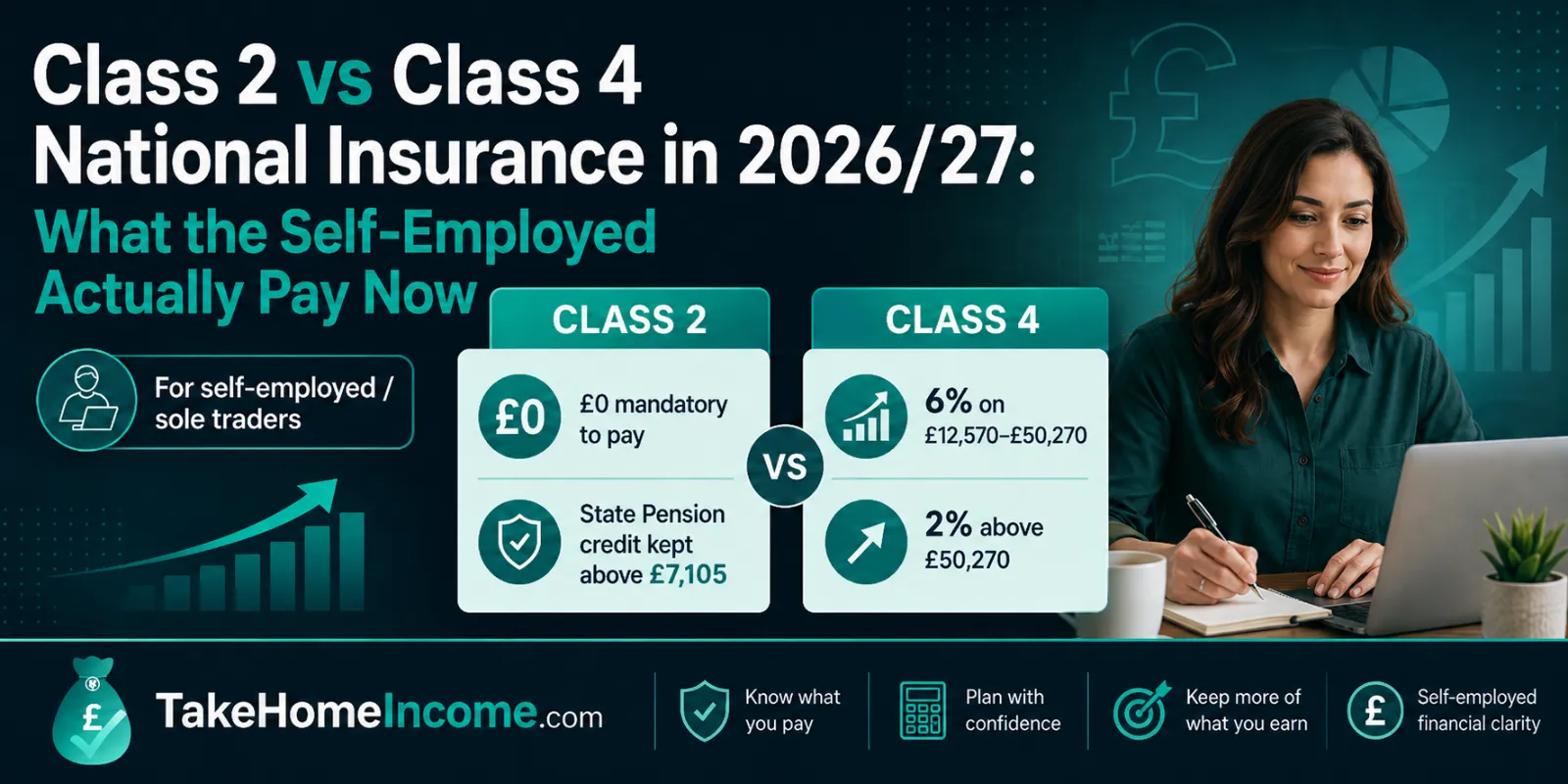

If you are self-employed, the short version for 2026/27 is this: you no longer pay Class 2 National Insurance as a separate bill, and Class 4 National Insurance is charged at 6% on the slice of your profit between £12,570 and £50,270 (then 2% above that). Class 2 has been effectively abolished as a mandatory charge – but as long as your profit is at or above the Small Profits Threshold of £7,105, you are still treated as having paid it, so you keep building your State Pension for free. This is the post-2024 reform that older articles still get wrong, so let us pin every number down.

Class 2 vs Class 4 National Insurance: the quick answer

The two classes do different jobs. Class 2 was a flat weekly contribution that protected your State Pension and benefit entitlements. Class 4 is a percentage charge on profit that raises revenue but historically gave you no extra benefits. Here is how they compare in 2026/27.

| Class 2 NIC | Class 4 NIC | |

|---|---|---|

| Who pays | Sole traders & partners (now credited, not charged) | Sole traders & partners |

| How it is charged | Flat weekly rate (£3.65/wk) | Percentage of taxable profit |

| 2026/27 rate | £0 to pay at/above the Small Profits Threshold | 6% main rate, then 2% |

| Key threshold | Small Profits Threshold £7,105 | Lower Profits Limit £12,570; Upper Profits Limit £50,270 |

| Builds State Pension? | Yes – treated as paid above £7,105 | No (revenue charge only) |

| Status now | Effectively abolished as a mandatory charge | Cut from 9% to 6%, still live |

So most sole traders now pay only Class 4, and only once profit clears £12,570. Class 2 sits quietly in the background as a free National Insurance credit. The same rules apply if you are a partner in a business partnership – your share of the profit is what counts towards each threshold.

What changed: Class 2 ‘abolished’ and the auto-credit

From 6 April 2024 the government scrapped compulsory Class 2 National Insurance for the self-employed, and that position carries into 2026/27. The word “abolished” is doing some heavy lifting, though – here is what actually happens now:

- Profit at or above £7,105 (the Small Profits Threshold): Class 2 is £0 to pay. You are treated as if you had paid it, so the year still counts towards your State Pension and contributory benefits. There is nothing to do and nothing to hand over.

- Profit below £7,105: nothing is charged automatically, but you can choose to pay voluntary Class 2 at £3.65 a week to protect that year of your record.

The practical effect is that the old separate “Class 2 line” on a Self Assessment bill has gone for the vast majority of sole traders. You do not opt in to the credit – HMRC applies it automatically when your Self Assessment return shows profit above the threshold.

What is the Class 4 National Insurance rate for 2026/27?

Class 4 is the one that still costs you money, and it is now noticeably cheaper than it used to be. The main rate was cut from 9% to 6%. For 2026/27 it works in two slices on your taxable profit:

- 6% on profit between the Lower Profits Limit (£12,570) and the Upper Profits Limit (£50,270).

- 2% on profit above £50,270.

- 0% on the first £12,570 of profit – you pay no Class 4 at all below that.

Like Income Tax, Class 4 only bites on the part of your profit inside each band. The most you can pay in the 6% band is on the full £37,700 between £12,570 and £50,270, which is £2,262 a year. Above £50,270 the marginal rate drops to just 2%, mirroring how employee National Insurance falls away at the higher end.

The thresholds that matter (and the £7,105 vs £12,570 confusion)

Three numbers do almost all the work for self-employed National Insurance in 2026/27. Mixing them up is the single biggest source of error online, so here they are side by side.

| Threshold | 2026/27 figure | What it does |

|---|---|---|

| Small Profits Threshold (SPT) | £7,105 | At/above this, Class 2 is treated as paid (free State Pension credit). Below it, Class 2 is voluntary. |

| Lower Profits Limit (LPL) | £12,570 | Where Class 4 actually starts. No Class 4 below this. |

| Upper Profits Limit (UPL) | £50,270 | Class 4 drops from 6% to 2% on profit above this. |

The key takeaway: a sole trader with profit between £7,105 and £12,570 pays no National Insurance of any kind yet still earns a qualifying year for the State Pension. You only start handing over cash – via Class 4 – once profit passes £12,570.

Voluntary Class 2: when paying below the threshold is worth it

If your profit is under £7,105 (or you made a loss), Class 2 is no longer charged – but you can still pay it voluntarily at £3.65 a week, about £189.80 for the full year. That tiny sum can be one of the best-value payments in the tax system, because it buys a qualifying year towards your State Pension. Consider paying voluntary Class 2 if:

- You are below the £7,105 threshold and this year would otherwise be a gap in your National Insurance record.

- You need 35 qualifying years (or close to it) for the full new State Pension and are short.

- You want to protect entitlement to certain contributory benefits, such as Maternity Allowance.

It is rarely worth paying voluntary Class 3 instead (far more expensive at over £17 a week) if you are eligible for the cheaper Class 2 rate. Check your National Insurance record on GOV.UK before paying, in case the year is already covered by employment or credits.

A worked example: National Insurance on £35,000 of profit

Take a sole trader in England with £35,000 of taxable profit (income after allowable expenses) in 2026/27, no student loan. Here is the full National Insurance and Income Tax picture, calculated band by band.

| Item | Working | Amount |

|---|---|---|

| Taxable profit | , | £35,000 |

| Income Tax | 20% on (£35,000 − £12,570 = £22,430) | −£4,486.00 |

| Class 4 NI (main rate) | 6% on (£35,000 − £12,570 = £22,430) | −£1,345.80 |

| Class 4 NI (2% band) | Profit below £50,270 | £0.00 |

| Class 2 NI | Profit above £7,105 → treated as paid | £0.00 |

| Total to HMRC | Income Tax + Class 4 | −£5,831.80 |

| Take-home profit | £35,000 − £5,831.80 | £29,168.20 a year |

That is about £2,431 a month, an effective deduction rate of roughly 16.7%. Notice that the entire National Insurance bill here is the £1,345.80 of Class 4 – there is no Class 2 to add. Under the old 9% rate, that same Class 4 slice would have cost £2,018.70, so the 6% cut saves this trader around £673 a year.

Both the Income Tax and the Class 4 National Insurance are collected together through Self Assessment, not deducted from each invoice the way PAYE works for employees. You report your profit on your tax return, and HMRC bills the combined amount. If your bill is large enough, HMRC may also ask for payments on account – advance instalments towards next year – though the totals above are the actual liability for the year itself, not the cash-flow timing.

Why was I charged Class 2 National Insurance ‘in error’?

This is a genuinely common, under-explained problem. After the reform, HMRC’s Self Assessment systems sometimes added a Class 2 charge that should not be there – typically because the National Insurance record or the ‘date you became self-employed’ was missing or mismatched, so the system did not recognise you as entitled to the free credit. If your 2026/27 calculation shows a Class 2 amount you did not expect, here is how to deal with it:

- Check your figure. For most traders the correct Class 2 amount to pay is £0. A charge of around £189.80 (52 × £3.65) usually means voluntary Class 2 has been applied when it should not be.

- Confirm HMRC has your self-employment registered. The credit relies on HMRC knowing the date your self-employment started. If you only registered recently, the National Insurance and Self Assessment records can be out of step.

- Contact HMRC’s National Insurance helpline to have the record corrected, then ask for your Self Assessment calculation to be recomputed. Many erroneous charges are removed once the self-employment start date is confirmed.

- Do not simply delete the line yourself if it is genuinely voluntary and you want the qualifying year – removing it could leave a gap in your record.

If in doubt, the official, free route is to ring HMRC and confirm whether the year is already covered. It is a known wrinkle of the transition, not something you did wrong.

Key takeaways

- Class 2 is effectively abolished as a mandatory charge – it is £0 to pay where profit is at or above the Small Profits Threshold of £7,105, but you are still credited towards the State Pension.

- Class 4 is the one you actually pay: 6% on profit between £12,570 and £50,270, then 2% above £50,270.

- The most you can pay in the 6% Class 4 band is £2,262 a year (6% of £37,700).

- You pay no National Insurance at all on profit below £12,570, yet profit between £7,105 and £12,570 still earns a qualifying year.

- Voluntary Class 2 below £7,105 costs about £189.80 a year (£3.65/week) and can be excellent value for protecting your State Pension.

- On £35,000 of profit, total National Insurance is just £1,345.80 (all Class 4); total to HMRC including Income Tax is £5,831.80.

Calculate your self-employed National Insurance and tax

Your own figure depends on your profit, region (Scotland has different Income Tax bands), allowable expenses, the £1,000 trading allowance and any student loan. Our UK self-employed tax calculator does the full 2026/27 calculation – Income Tax, Class 4 and Class 2 status – and shows the working line by line so you can see exactly where each pound goes.